Policy Priorities

For more than 25 years, Oweesta Corporation has been dedicated to strengthening financial systems in Indian Country through capacity building and access to capital, primarily in service to Native CDFIs and Tribal communities.

In 2024, Oweesta’s Board of Directors adopted an updated strategic plan that guides the next five years of our commitment to this work. A central component of this plan is the formation of an internal advocacy team to advance public policies that support Oweesta’s role as a national Native CDFI intermediary and funder.

Below are the mission-aligned policy priorities we believe are essential to sustaining and strengthening our ability to serve Native CDFIs, Tribes, and the communities they support.

Oweesta Corporation is a national Native community development financial institution (CDFI) intermediary dedicated exclusively to serving Native CDFIs and Native communities, which includes Native American, Alaska Native, and Native Hawaiian peoples.

Our mission is to create pathways for Native people to build financial assets, generate wealth, and strengthen sovereignty through the development of strong, sustainable institutions and programs.

Native CDFIs occupy a distinct and vital place within the national financial and policy landscape. As Native-led institutions, we are rooted in sovereignty and operate within a unique federal relationship grounded in the U.S. Constitution, treaties, and federal trust responsibilities. This relationship establishes a government-to-government framework that recognizes the inherent rights of Tribal Nations and Native peoples—not as beneficiaries of diversity initiatives, but as sovereign governments and communities with enduring political and economic rights.

Through training, technical assistance, investment, research, and policy advocacy, Oweesta strengthens access to capital and supports the development of culturally grounded financial systems. Our advocacy centers on advancing Oweesta’s mission and expanding the reach of our programs and investments—work that, in turn, empowers Native CDFIs and Native communities across Indian Country, Alaska, and Hawai‘i to build lasting economic independence and community wealth.

Our policy priorities reflect this foundation. Oweesta advocates for federal policies that honor sovereignty, increase access to equitable capital, and invest in Native financial institutions as essential partners in economic development and nation building.

To help to achieve our mission, Oweesta recommends the following actions:

U.S. Department of the Treasury

- Congress should appropriate $50 million in FY26 for the Native American CDFI Assistance (NACA) program under the U.S. Department of the Treasury’s CDFI Fund.

- Congress should enact the CDFI Bond Guarantee Improvement Act of 2025 to extend authorization for the CDFI Bond Guarantee Program for four years and expand access to it by reducing the minimum loan size to $25 million and removing the annual limit on guarantees, allowing smaller rural and Native CDFIs to utilize the program and to support more community development projects.

- Congress should enact the Scaling Community Lenders Act, which authorizes the Treasury Secretary to use dividends from the Emergency Capital Investment Program to fund the CDFI liquidity enhancement pilot program to fund private sector liquidity facilities that help to expand the lending capacity of CDFIs.

- Congress should enact the Inspiring Nationally Vibrant Economies Sustaining Tribes Act (INVEST Act), which establishes a set percentage of annual New Market Tax Credit allocations to be directed to competitive Native Community Development Entities (CDEs) to originate transactions in Tribal communities, accompanied by technical assistance resources.

- The CDFI Fund should contract with Native-led organizations to expand training and technical assistance offerings for Native CDFIs to maximize their ability to access seed capital, achieve certification/recertification, and promote the self-sufficiency and sustainability of small and emerging Native CDFIs.

- The CDFI Fund should streamline its certification process to allow certification and recertification applicants to cure non-substantive deficiencies by providing a set time period to correct minor errors or provide missing documentation without having to re-apply entirely.

- The CDFI Fund should assign priority points for projects on tribal land through the Capital Magnet Fund to increase access to gap financing in under-resourced rural and tribal communities.

U.S. Department of Housing and Urban Development

- HUD should designate at least 10% of its Comprehensive Housing Counseling funding to support housing counseling programs in tribal areas, including through HUD-approved housing counseling intermediaries supporting Native-led housing counseling agencies.

- Congress should reauthorize the Native American Housing Assistance and Self-Determination Act of 1996 (NAHASDA) and appropriate $1.1 billion for Indian Housing Block Grant (IHBG) funding and $35 million for the Native Hawaiian Block Grant.

- Congress should appropriate at least $50 million for HUD’s Section 4 Capacity Building for Community Development and Affordable Housing Program and ensure that at least 10% is invested in tribal areas, as required by law.

- Congress should appropriate $148 million to NeighborWorks America with at least 10% of the funding dedicated to existing and new tribal organizations in the NeighborWorks member organization network.

U.S. Department of Agriculture (USDA)

- Congress should appropriate at least $10 million for the USDA 502 Native CDFI Relending Demonstration program and permanently authorize the program, which has successfully increased the flow of affordable mortgage capital to eligible borrowers on tribal land.

- USDA should assign priority points and waive match requirements for the Rural Community Development Initiative (RCDI) from qualified, Naive-led intermediary organizations.

- USDA should assign priority points for proposals that support Indigenous food systems through the Local Food Purchase Assistance Cooperative Agreement (LFPA) and LFPA Plus programs to purchase local foods from local, regional, underserved, and Tribal producers to distribute those foods to their communities.

- USDA should continue the Indigenous Animals Harvesting and Meat Processing Grant Program (IAG).

U.S. Department of Health & Human Services (HHS)

Congress should support continued funding for the Administration for Native Americans (ANA) Social and Economic Development Strategies (SEDS) program and CDFI preference.

U.S. Department of Interior (DOI)

- Congress should enact the Tribal Trust Land Homeownership Act of 2025 to modernize the Bureau of Indian Affairs (BIA) residential leasing, mortgage approval, and Title State Report (TSR) processes to enhance access to mortgage capital on trust lands.

- DOI’s Bureau of Indian Education (BIE) should contract with Native-led youth financial education providers to provide basic financial management skills to students through BIE schools.

- DOI should explore strategies to increase housing and economic development on tribal land through existing Memorandum of Understanding (MOUs) with Native-led intermediaries.

U.S. Department of Veterans Affairs (VA)

The VA Department should expedite rulemaking for the Native American Direct Loan Improvement Act of 2023, as enacted in the Senator Elizabeth Dole 21st Century Veterans Healthcare and Benefits Improvement Act and continue its 2.5% interest rate reduction pilot to increase access to mortgage finance for eligible Native American veteran borrowers on tribal land.

Federal Bank Regulators

The Federal Reserve Board of Governors, Office of the Comptroller of the Currency, and

the Federal Deposit Insurance Corporation should provide a mechanism for financial institutions to receive positive consideration under the Community Reinvestment Act for lending and investments in tribal communities, even if the activity is not located in the institution’s service area.

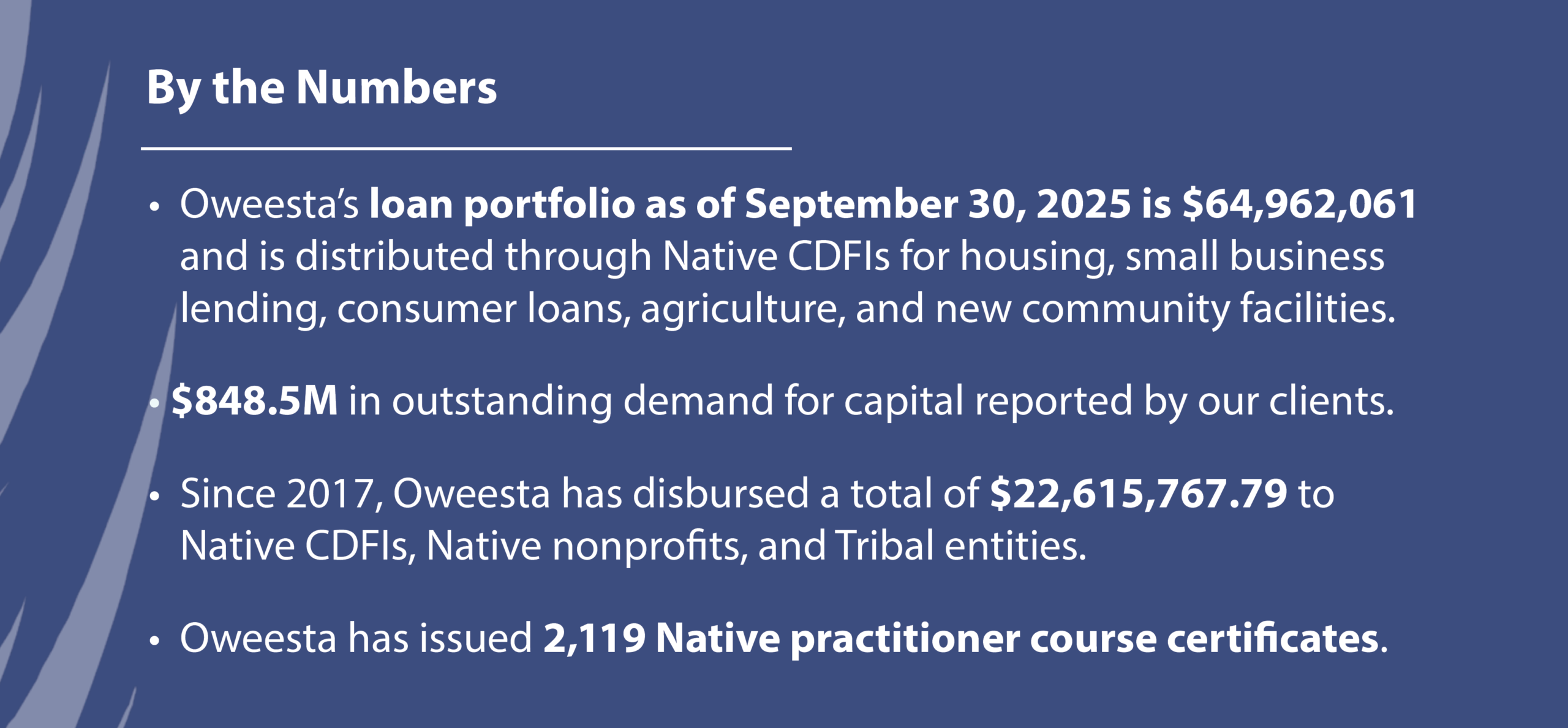

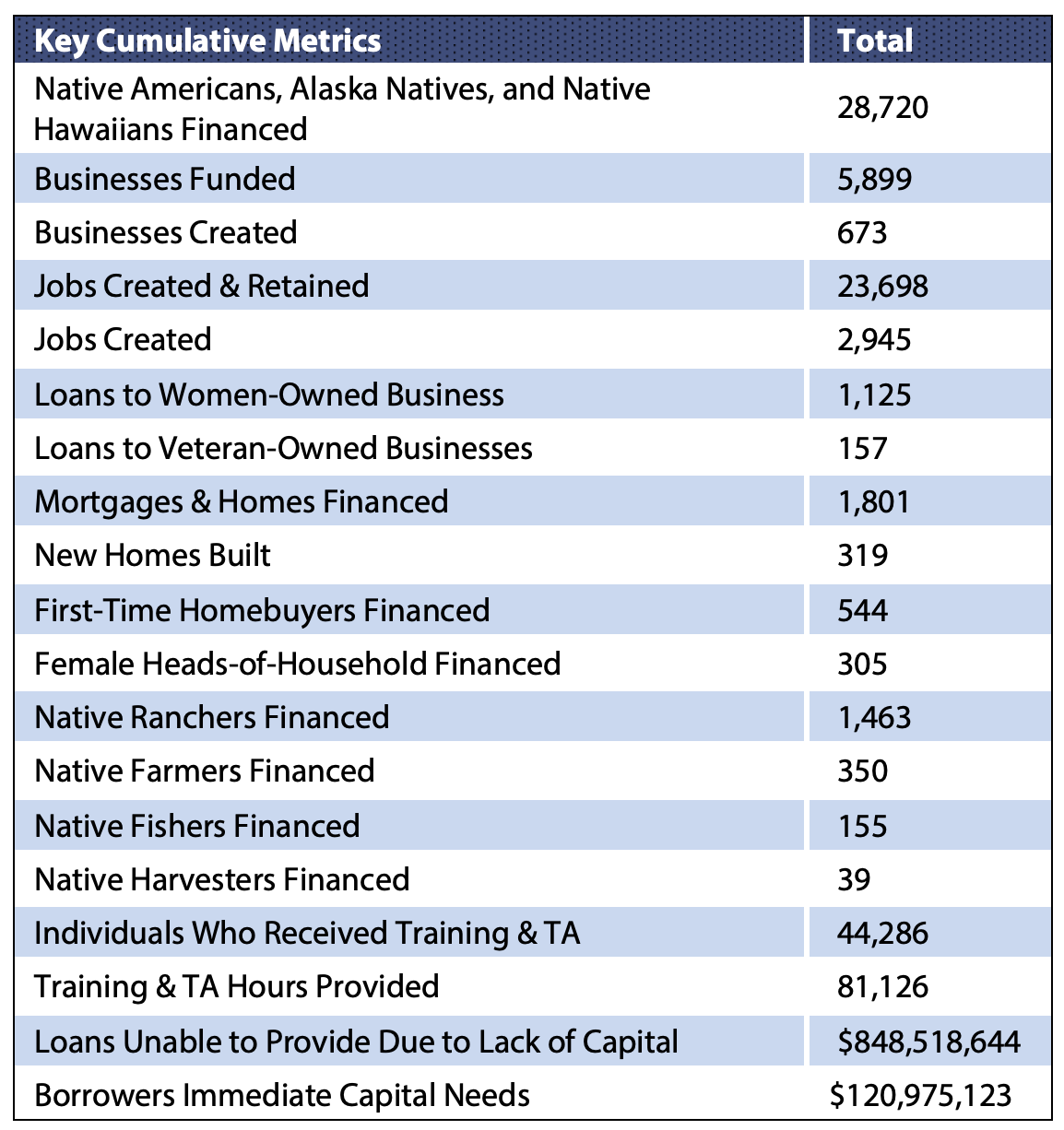

OWEESTA CORPORATION’S CUMULATIVE IMPACT

In its impact tracking, Oweesta receives information from its borrowers about the loan types disbursed and the demographics of end borrowers who receive financing. Details of the cumulative data collected from borrowers’ quarterly reports is listed below. Since Oweesta began lending, our borrowers have disbursed 38,899 loans totaling $1,368,011,680.

Click to download Oweesta’s Policy Priorities.